FATCA: What You Need to Know

The US government discourages its citizens from owning or investing in offshore financial assets by imposing strict reporting requirements on those who do. Not only are most investors required to file an annual report known as the FBAR with the Financial Crimes Enforcement Network, they are also required to file a report with the IRS under the Foreign Account Tax Compliance Act (FATCA).

We’ve already discussed how FBAR reporting affects US individuals and businesses, so today let’s look at FATCA and see how these compliance requirements will impact those with foreign financial assets.

What is FATCA?

The Foreign Account Tax Compliance Act — FATCA, for short — is a law that Congress passed in 2010 to help US authorities fight tax evasion. Under FATCA, US taxpayers are required to file annual tax forms that report balances of and activity in their offshore financial holdings. Foreign financial institutions who hold assets belonging to US taxpayers also have compliance requirements under FATCA.

FATCA compliance is overseen by the IRS, which is a division of the Treasury Department. This gives the IRS enforcement authority and the power to impose penalties on folks and institutions who fail to comply.

Who Needs to Comply with FATCA?

FATCA impacts two categories of people or institutions: (1) those who invest in offshore financial institutions, and (2) the foreign financial institutions themselves. Let’s discuss both.

FATCA for Investors

You must comply with FATCA if all the following are true:

1. You are a specified individual or a specified domestic entity.

Specified individuals are any of the following:

- A US citizen

- A US resident alien

- A US nonresident alien who made an election to be treated as a resident alien for tax purposes

- A US nonresident alien who is a bona fide resident of American Samoa or Puerto Rico

Specified domestic entities are any of the following:

- A closely held domestic corporation or partnership that gets at least 50% of its income from passive sources

- A closely held domestic corporation or partnership if at least 50% of its assets produce (or are held for the production of) passive income

- A domestic trust described in section 7701(a)(30)(E) that has one or more specified persons as a current beneficiary

2. You file a US tax return.

Individuals and businesses that don’t file US tax returns or informational reports will be exempt from filing the annual FATCA report in most instances.

3. You have interest in specified foreign financial assets.

This includes bank accounts, checking accounts, brokerage accounts, options accounts, cash-value insurance policies, mutual funds, and nearly any other financial account maintained in a jurisdiction other than the United States or a US territory.

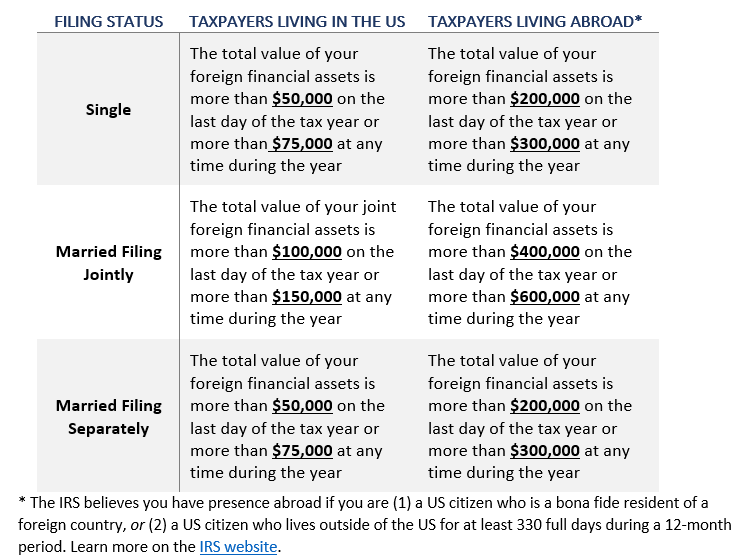

4. Your foreign financial assets exceed the reporting thresholds.

The reporting thresholds vary depending on the type of specified person you are, where you live, and your filing status. For example, expats who live abroad have higher reporting thresholds than taxpayers living on US soil because the IRS recognizes that — logistically — an expat will need a bank account in the country where they are living and working.

Below is a table that shows the reporting thresholds for each type of individual taxpayer. If you exceed these thresholds, you must file the annual FATCA tax form.

If you are a specified domestic entity, you will reach the reporting threshold for FATCA if the total value of your foreign financial assets is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year.

FATCA for Financial Institutions

US taxpayers aren’t the only ones required to comply with FATCA. Foreign financial institutions (FFIs) and certain non-financial foreign entities (NFFEs) are obligated to report information about their US customers and account holders. Each jurisdiction’s requirements are different, but most FFIs will need to report:

- The identity of their US customers (e.g., name, address, taxpayer identification number, etc.)

- Account numbers and account balances owned by those US customers

- Annual earnings on those accounts (e.g., interest, dividends, royalties, etc.)

FATCA FAQs

If you have offshore bank accounts or foreign investments that exceed the filing thresholds, we want assure you that FATCA compliance is manageable. It may seem overwhelming at first, but once you understand what’s required of you, the compliance requirements won’t seem as onerous.

Here are some of the most commonly asked questions our firm gets about FATCA.

How do US taxpayers report information under FATCA?

US taxpayers should file IRS Form 8938 to fulfill their FATCA reporting responsibilities.

What’s in the FATCA tax form?

Form 8938 asks for detailed information about your foreign financial assets, including the following:

- The number of offshore accounts you own

- The value of your foreign financial assets

- Earnings from your foreign financial assets, especially those that could be taxable

- Information about the deposit and custodial accounts themselves (e.g., name and mailing address of financial institution, the maximum value of your account during the year, the type of currency your account uses, etc.)

When is the FATCA report due?

You should file Form 8938 with your annual income tax return or informational return.

Can I get a filing extension?

If the IRS grants you an extension to file your annual income tax return, you will automatically receive an extension to file Form 8938.

What happens if I don’t comply with FATCA?

If you fail to file Form 8938, you may be subject to a penalty of up to $10,000. If you continue to ignore IRS notices about your filing responsibility, this penalty could jump to $50,000. If you underpay the taxes assessed on your foreign accounts, you could incur a penalty equal to 40% of the tax you owe.

Maintaining foreign investments requires you to jump through a few hoops, but we think these requirements are manageable, especially if you have help from a team you trust. At AB FinWright, we love to work with people who operate cross-border businesses or individuals who live and/or work overseas. If you want to learn how we can help you manage these filing requirements, contact us for a consultation. We’d love to help make your life a bit easier.